Share This Article

In this article

When Canadian businesses set their sights on U.S. expansion, they're stepping into a financial battlefield where one wrong move can cost millions.

The U.S. market isn't just another North American territory—it's an ecosystem with financial rules that can trap the unprepared.

State-by-state tax variations create a regulatory minefield where strategies that work in one region can fail in another.

Currency volatility turns profit margins into a high-stakes game, and capitalization expectations demand far more than most Canadian firms anticipate.

What sounds like a promising growth strategy can quickly become an expensive lesson in financial miscalculation.

This guide breaks down the biggest financial mistakes Canadian businesses make when expanding to the U.S.—and how to avoid them.

Methodology

All the numbers and facts here come straight from the source:

Key Takeaways

- U.S. banking operates differently—opening a business bank account can be complex, and payment processing relies more on checks and ACH transfers.

- Merchant fees for credit card transactions are higher in the U.S. compared to Canada, affecting profitability.

- U.S. tax regulations vary by state, and sales tax compliance is different from Canada’s national VAT system.

- Failing to comply with IRS and state tax rules can lead to penalties and unexpected financial burdens.

- The CAD/USD exchange rate fluctuates, and ignoring FX risks can erode profit margins.

- Cross-border banking fees and hidden charges significantly increases transaction costs.

- FX hedging strategies help mitigate risk, yet many businesses overlook them, exposing themselves to financial volatility.

- U.S. businesses follow different invoicing norms, such as Net 30 or Net 60, which can cause cash flow gaps.

- Delayed B2B payments are common, making it harder for businesses to maintain steady cash flow.

#1. Failing to Adapt to U.S. Banking and Payment Infrastructure

Banking in the U.S. and Canada follows a similar process, but there are key differences to be aware of.

Both countries require proper business registration, essential documents, and compliance with anti-money laundering (AML) regulations.

However, U.S. banks often have stricter verification processes, sometimes requiring a physical U.S. address and an Employer Identification Number (EIN).

Some banks may also request an in-person visit to open an account, which can add logistical challenges for foreign business owners.

Additionally, international transactions in the U.S. may experience longer processing times and higher fees compared to domestic transactions.

Payment Processing in U.S. Works Differently

Canada relies heavily on Interac, where instant money transfers are standard.

In the U.S., checks remain common in B2B transactions, and ACH (Automated Clearing House) transfers—comparable to Canada’s EFT—take days to clear rather than being near-instant.

Credit card fees are another major difference.

In Canada, interchange fees are capped. In the U.S., they aren’t—meaning small businesses can face transaction fees.

For Canadian businesses expanding into the U.S., failing to anticipate these differences can lead to unexpected costs, delayed payments, and frustrated customers.

Overlooking Complex U.S. Tax Obligations

In Canada, tax is relatively straightforward. There’s a federal corporate tax rate and a harmonized sales tax (HST/GST) system.

You collect sales tax at the point of sale, remit it to the government, and that’s that.

The U.S.? different game entirely.

Sales Tax

The U.S. doesn’t have a national sales tax like Canada’s GST/HST. Instead, each state sets its own rates and rules—and there are 50 of them.

Some states have no sales tax (e.g., Oregon and New Hampshire). Others, like California, have a base rate plus local taxes that can push total sales tax over 10.75%.

There’s no automatic registration like in Canada. Businesses need to determine where they have nexus—a legal term that defines whether they owe sales tax in a given state.

Sell enough in a state and you could be on the hook for collecting, filing, and remitting sales tax there.

Fail to comply? Audits. Penalties. Headaches.

Federal and State Corporate Tax Compliance

Canada has a single federal corporate tax return. The U.S. has two levels—federal and state.

The IRS (Internal Revenue Service) handles federal taxes, but each state has its own tax rules, rates, and filing requirements—some states (like Texas) don’t have a corporate income tax, while others (like New York) impose both corporate income and franchise taxes.

If your business operates in California and New York, you could owe taxes in both.

Many Canadian businesses get caught off guard, assuming that registering in one state means they only owe tax there.

They don’t realize that selling into multiple states could trigger multi-state tax filings—a compliance nightmare if unprepared.

Misunderstanding the Canada-U.S. Tax Treaty

Canada and the U.S. have a tax treaty to prevent double taxation—but it doesn’t mean businesses are exempt from filing U.S. taxes.

Some businesses assume that if they pay tax in Canada, they won’t owe U.S. tax—wrong. The IRS still requires reporting, even if the treaty eliminates some tax liability.

The treaty also has permanent establishment rules, meaning if your company has a U.S. office, employees, or significant operations there, you could owe U.S. corporate tax even if your HQ is in Canada.

#2. Choosing the Wrong Legal Structure for U.S. Expansion

When expanding into the U.S., you’ll need to structure your business correctly. The legal entity you choose impacts your tax burden, liability, and long-term flexibility.

Get it wrong, and you could face higher taxes, legal exposure and unnecessary administrative costs.

Many Canadian businesses default to what seems easiest or cheapest, only to realize later that they’ve locked themselves into double taxation, complex compliance requirements, or excessive state fees.

LLC, C-Corp, or S-Corp? Making the Right Choice Matters

The U.S. offers multiple business structures, each with different tax implications and liabilities. Selecting the wrong one can significantly impact profitability.

Limited Liability Company (LLC)

- Tax Treatment: Pass-through taxation—profits flow directly to owners’ personal tax returns.

- Best For: Small businesses, freelancers, and those looking to avoid corporate taxation.

- Risks for Canadians: Canada doesn’t recognize the LLC’s pass-through status, meaning profits can be taxed twice—once in the U.S. and again in Canada. Despite roughly 21.6 million LLCs in the United States, they often create tax headaches for Canadian business owners.

C-Corporation (C-Corp)

- Tax Treatment: Pays corporate tax separately (21% federal rate + state taxes).

- Best For: Startups raising venture capital or businesses reinvesting profits.

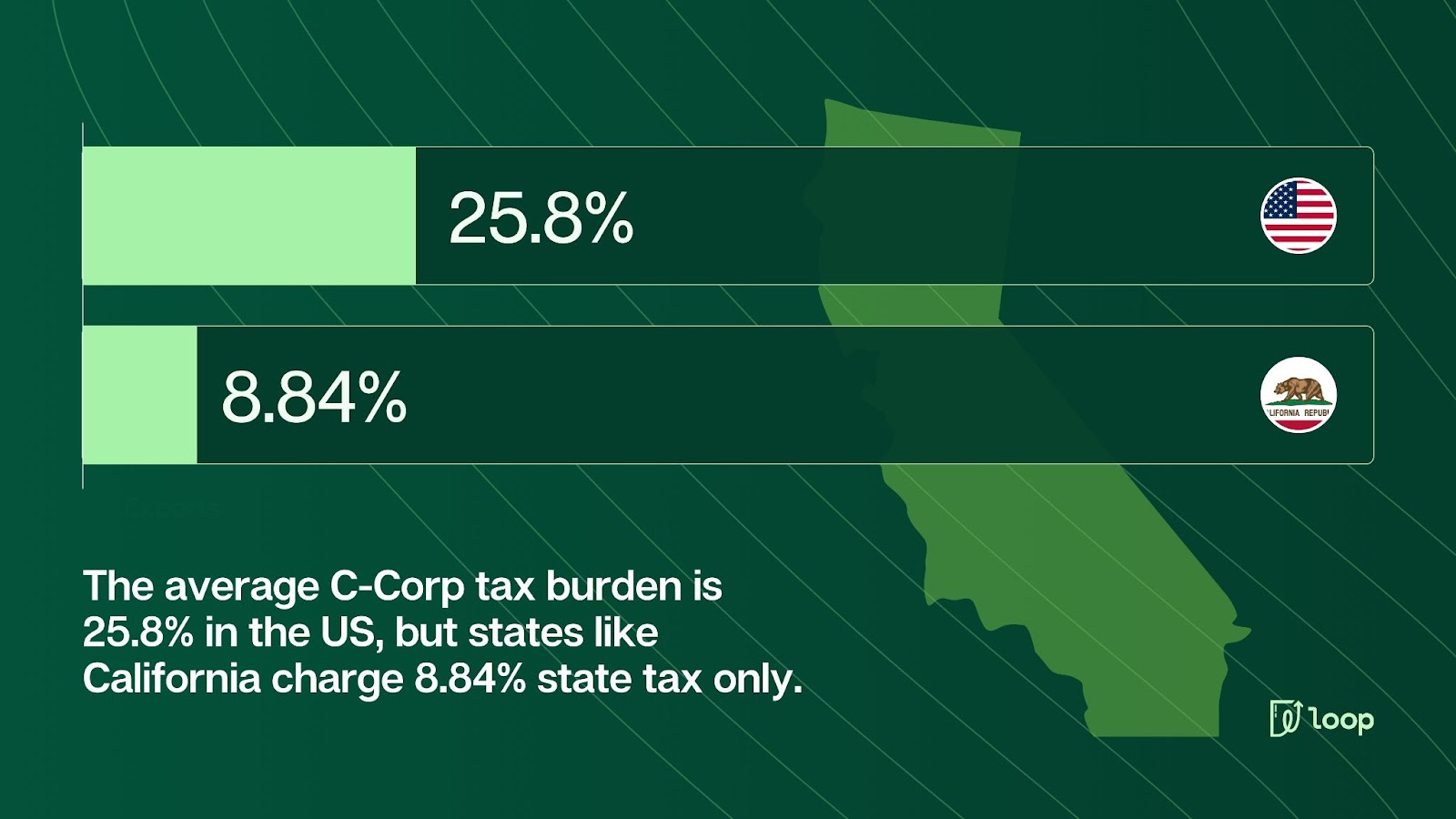

- Risks: Subject to double taxation—profits are taxed at the corporate level and again when distributed as dividends. The average total corporate tax burden (federal + state) is 25.8%, but in states like California, it is 8.84% for state tax only.

S-Corporation (S-Corp)

- Tax Treatment: Pass-through taxation, avoiding double taxation.

- Best For: U.S. based small businesses looking for tax efficiency.

- Risks for Canadians: Non-U.S. residents cannot own S-Corps, making this option unavailable for Canadian businesses.

Registering in the Wrong State Can Increase Costs

Where you incorporate matters. Many Canadian businesses assume they should register in a business-friendly state like Delaware—but that’s not always the best choice.

- Delaware: Ideal for large corporations and startups raising VC funding due to flexible corporate laws. However, if you operate in another state, you must register there too, leading to additional fees and compliance costs.

- California: High corporate taxes (8.84%) and franchise fees make it one of the most expensive states for incorporation.

- Wyoming and Nevada: No state corporate tax, but operating from Canada still triggers U.S. tax liabilities.

Over 67.6% of Fortune 500 companies are incorporated in Delaware, for small businesses, the extra compliance costs may outweigh the benefits.

Double Taxation Risks Can Erode Profits

C-Corps face double taxation—once at the corporate level and again on dividends.

LLCs create uncertainty since Canada doesn’t recognize U.S. pass-through taxation. Tax treaty relief exists, but businesses must file correctly to avoid unnecessary taxes.

#3. Ignoring Foreign Exchange Volatility and Currency Risks

Expanding into the U.S. means navigating foreign exchange (FX) risks that can erode profit margins if not properly managed.

Many Canadian businesses assume the CAD/USD exchange rate will remain stable, but history suggests otherwise.

Ignoring currency fluctuations, hidden banking fees and a lack of FX hedging strategies can lead to unexpected losses, uncompetitive pricing, and cash flow instability.

The CAD/USD Exchange Rate Is Highly Volatile

The Canadian dollar (CAD) is among the most volatile major currencies, influenced by oil prices, interest rate differentials and global economic conditions.

This volatility directly impacts revenue, pricing, and profitability for businesses transacting in U.S. dollars.

- Over the past five years, the CAD/USD exchange rate has fluctuated between $0.69 and $0.82.

- The Bank of Canada projects continued fluctuations due to inflationary pressures and geopolitical factors.

- A 5% depreciation in the CAD translates to a $50,000 loss on every $1M in revenue if businesses fail to adjust for exchange rate changes.

Hidden Banking Fees Can Erode Margins

Cross-border transactions come with hidden costs that many businesses overlook. Banks add markups, processing fees and wire charges, significantly reducing overall profitability.

- FX conversion markups: Canadian banks typically charge 1-3% above mid-market rates, cutting into revenue.

- Wire transfer fees: U.S. banks charge between $15 to $50 per transfer, depending on the institution.

- Merchant processing fees: Accepting CAD-to-USD payments via credit card adds an extra 1-3% per transaction.

A Canadian e-commerce brand selling $1M USD annually could lose over $30,000 in unnecessary FX fees simply by relying on standard bank transfers.

Lack of FX Hedging Leads to Financial Instability

Many businesses fail to hedge against FX risk, exposing themselves to revenue losses when the exchange rate moves against them.

Key FX risk management tools include:

- Forward Contracts: Lock in an exchange rate for future transactions to mitigate currency depreciation risks.

- Multi-Currency Accounts: Hold U.S. dollars to avoid unnecessary conversions.

- Automated FX Platforms: Use a fintech providers like loop to access better exchange rates than traditional banks.

#4. Expanding Without a Solid Cash Flow Strategy

Expanding into the U.S. requires adapting to different payment cycles and cash flow norms.

Failing to account for longer payment terms, delays in B2B transactions and difficulties in accessing short-term financing create cash flow gaps that threaten operations.

U.S. Payment Cycles Are Longer

Unlike Canada, where Net 30 is standard, many U.S. companies operate on Net 45 or even Net 60 payment terms—meaning payments arrive much later than expected.

- Most U.S. businesses use Net 45 or longer payment terms.

- B2B enterprises wait 40.3 days on average to receive payments (compared to 30 days in Canada).

Delayed B2B Payments Can Create Liquidity Issues

In the US, 64% percent of companies face delayed payments, with suppliers typically waiting an average of 43 days to receive funds.

Unlike consumer transactions, B2B payments in the U.S. are often delayed due to complex approval processes, cash flow management tactics, and industry norms.

Difficulty Securing Short-Term Financing

Cash flow gaps can be bridged with short-term financing, but Canadian businesses expanding to the U.S. often struggle to access credit facilities due to a lack of U.S. financial history.

- Traditional banks require a U.S. credit history before approving loans or credit lines.

- Alternative lending solutions (e.g., invoice factoring, revenue-based financing) charge higher fees.

#5. Struggling to Secure Financing Due to Lack of U.S. Credit History

Another financial hurdle for Canadian businesses expanding to the U.S. is establishing credit.

Many assume that their Canadian credit history will transfer, but U.S. banks and lenders do not recognize Canadian credit scores.

No U.S. Credit History = Limited Access to Business Loans

Without a U.S. credit profile, banks and financial institutions view Canadian companies as high-risk borrowers, significantly reducing loan approval chances.

- U.S. banks typically require at least 2 years of U.S. business financials before offering traditional business loans.

- SBA loans (Small Business Administration) are often unavailable to businesses without a U.S. credit footprint.

Higher Interest Rates on Financing

Even if Canadian businesses get approved for financing, interest rates are often significantly higher due to their lack of U.S. credit.

- Average interest rates for U.S. small business loans range from 6.43% to 12.45%, but foreign businesses often see higher rates.

- Alternative lending platforms (like merchant cash advances or revenue-based financing) charge even more.

Difficulty Securing U.S. Corporate Credit Cards

U.S. corporate credit cards are essential for managing operational expenses, travel, and vendor payments—but they require a U.S. credit profile.

- Most U.S. business credit card issuers require a FICO score of 700, which Canadian businesses do not have.

- Without a U.S. credit score, businesses often need to put down a cash deposit or have a U.S.-based guarantor.

- Limited credit options mean businesses miss out on cashback, rewards, and expense management benefits.

#6. Not Factoring in Compliance Costs

Expanding into the U.S. comes with significant regulatory and compliance expenses that many Canadian businesses underestimate.

Regulatory Filings Can Be Expensive and Time-Consuming

Before operating in the U.S., businesses must register with multiple federal and state agencies, which involves filing fees, legal expenses, and ongoing compliance costs.

- Employer Identification Number (EIN): Required for tax purposes and banking, issued by the IRS for free.

- State Business Registration: Filing fees vary from $50 (Missouri) to $800 (California).

- Foreign Qualification Fees: The average state fee to qualify a business corporation is $230, while the average fee to qualify a limited liability company (LLC) is $190.

Payroll Tax & Employment Regulations Differ by State

Hiring U.S. employees adds another layer of complexity, as payroll taxes, worker classification, and labor laws vary by state.

- Federal Payroll Taxes: Employers must pay 7.65% of wages for Social Security and Medicare taxes.

- State Unemployment Taxes (SUTA): Ranges from 0.1% to 12.65% of employee wages, depending on the state.

- Workers' Compensation Insurance: Mandatory in all states except Texas, costing between $0.95 per $100 in payroll.

Legal and Financial Audits Are Costly but Necessary

To stay compliant, businesses must regularly file financial reports, conduct audits, and maintain proper tax records.

- Annual Franchise Taxes: Some states, like Delaware and California, require businesses to pay annual franchise taxes of $175 and $800 minimum.

- Financial Statement Audits: Required for specific industries (e.g., finance, healthcare), costing between $20,000 and $50,000 per audit.

- IRS and State Tax Audits: Mistakes in tax filings can trigger audits, with penalties ranging from 5% to 25% of unpaid taxes.

#7. Mispricing Products for the U.S. Market

Many Canadian businesses assume their pricing models will work in the U.S. without considering the higher operational costs, state tax variations, and different consumer spending habits.

Failing to adjust pricing can erode profit margins, drive away customers, or make products uncompetitive in the U.S. market.

Higher Operational Costs in the U.S.

Expanding into the U.S. often comes with higher business expenses, including labor costs, rent, insurance, and logistics. Pricing that works in Canada may not cover the full costs of operating in the U.S.

- Commercial Rent: Retail and warehouse rent in U.S. cities like New York and San Francisco can be 30%-50% higher than in Toronto or Vancouver.

- Health Insurance: Unlike Canada, U.S. businesses must provide private health insurance for employees, adding an average of $7,739 per employee per year.

State Sales Tax Variances Affect Pricing Strategy

Unlike Canada’s federal GST/HST system, the U.S. has no national sales tax—instead, sales tax is determined at the state, county, and city levels, creating complex price variations.

- Five states (Oregon, Montana, New Hampshire, Delaware, and Alaska) have NO sales tax.

- California has the highest sales tax (up to 10.75%), while other states have rates between 4%-7%.

- Sales tax thresholds vary: Businesses selling over $100,000 or 200 transactions annually in a state must collect and remit sales tax.

Consumer Spending Habits Differ

U.S. consumers have different price sensitivities, purchasing power, and expectations compared to Canadians.

- Americans are more price-sensitive: A 2023 McKinsey report found that 78% of U.S. consumers actively search for discounts and compare prices before purchasing.

- Subscription and financing models are more popular in the US.

- Brand perception matters: Many U.S. consumers equate higher prices with higher quality, while Canadians tend to prefer value-driven pricing.

#8. Not Understanding the U.S. Funding and Investment Landscape

Many Canadian businesses assume funding, venture capital and business loans work the same way in the U.S. as they do in Canada.

This misunderstanding can limit financing options, create fundraising roadblocks, and make securing capital much harder in a competitive market.

Different Venture Capital Expectations

U.S. venture capitalists (VCs) operate with different expectations and risk appetites compared to Canadian investors.

U.S. investors focus more on rapid scaling rather than long-term sustainability. Startups are expected to burn cash aggressively to gain market share.

Higher valuation expectations: U.S. startups typically receive higher valuations compared to Canadian counterparts, leading to tougher negotiations for foreign businesses.

Preference for Delaware C-Corps: Many VCs prefer investing in U.S.-registered corporations, especially Delaware C-Corps, due to favorable tax laws and investor protections.

Difficulty Accessing SBA Loans

The U.S. Small Business Administration (SBA) offers loans with low interest rates and favorable repayment terms, but Canadian-owned businesses often don’t qualify.

SBA loans are restricted to businesses with U.S. ownership (typically requiring at least 51% U.S. citizen or permanent resident ownership).

Even Canadian subsidiaries in the U.S. often don’t qualify unless they meet specific residency and operational requirements.

Alternative financing (such as revenue-based financing and venture debt) is more common for foreign businesses.

Higher Investor Competition

The U.S. has a much larger and more competitive funding environment, making it harder for foreign businesses to stand out.

U.S. investors are flooded with pitches, making it crucial for foreign businesses to differentiate themselves with strong traction, U.S.-based operations, and market fit.

More emphasis on connections: In Canada, many funding opportunities are relationship-driven, whereas in the U.S., businesses must actively network, attend investor events, and build credibility.

#9. Failing to Account for High U.S. Labor and Employee Costs

Expanding to the U.S. means hiring under a completely different labor and payroll system—one that is far more expensive and complex than Canada’s.

Many Canadian businesses fail to account for higher employer payroll taxes, costly benefits, and varying state labor laws, leading to unexpected financial strain and compliance risks.

Higher Employer Payroll Taxes

Unlike Canada, where payroll taxes are relatively standardized, the U.S. system includes multiple employer-paid taxes that vary by state and federal level.

- FICA (Federal Insurance Contributions Act): Employers must pay 7.65% of an employee’s wages for Social Security (6.2%) and Medicare (1.45%).

- FUTA (Federal Unemployment Tax Act): Employers pay 6.0% on the first $7,000 of each employee’s wages, though tax credits can reduce this to 0.6%.

- SUTA (State Unemployment Tax Act): State unemployment tax rates range from 0.1% to 12.65%, depending on the state and the employer’s history of layoffs.

Expensive Employee Benefits (Healthcare, 401(k) Plans)

Unlike Canada, where healthcare is government-funded, U.S. employers must offer private health insurance—one of the biggest cost drivers for businesses.

- Average employer healthcare cost: $23,968 per employee per year for family coverage and $8,435 for single coverage (KFF, 2023).

- 401(k) retirement plans: Many U.S. employers offer 401(k) plans, which increases labor costs.

- Workers’ compensation insurance: Costs vary by state and industry, ranging from $0.75 to $2.74 per $100 in payroll.

Complex Labor Laws by State

U.S. labor laws vary significantly across states, making compliance more challenging than in Canada.

- Minimum wage differences: Federal minimum wage is $7.25/hour, but states like California ($16.00) and New York ($16.00) have much higher rates.

- At-will employment: In most states, employers can terminate employees without cause, but some states (e.g., Montana) have exceptions that require just cause.

- Paid leave laws: Unlike Canada, there is no federally mandated paid vacation or parental leave in the U.S., but states like California and New York require paid sick leave.

#10. Waiting Too Long to Bank on Loop

We had to include this one because it’s one of the easiest mistakes to avoid.

Too many Canadian businesses expand into the U.S. without a financial strategy built for cross-border operations.

They assume their current setup will work—but then come the costly FX conversions, cash flow gaps, and struggles to establish U.S. credit.

That’s why smart businesses call Loop early.

Loop offers a comprehensive suite of solutions tailored for businesses like yours:

- Low-Cost FX Transfers: Eliminate between 1-5% in FX fees on all cross-border payments, ensuring more of your revenue stays with you.

- Multi-Currency Corporate Credit Cards: Access corporate credit that scales with your business performance, allowing you to spend in multiple currencies without additional fees.

- Local U.S. Bank Accounts: Open local accounts to send and receive payments in the U.S., EU, and UK for free, eliminating double conversions and simplifying transactions.

By partnering with Loop, you can navigate the complexities of U.S. expansion with confidence, ensuring your financial operations are as seamless and efficient as possible.

Financial hurdles can impede your U.S. growth. Don’t allow that to happen. Contact Loop today and make your business cross-border expansion a success.

This is a brief blurb that should summarize what loop does. Maybe it will serve as a brief intro to some of the features?